While planning finances for the year 2026, Canadians generally struggle with two favorites: RRSP vs TFSA 2026. Both are effective ways to accumulate wealth. Nonetheless, considering the different mechanisms, it is up to your goals, income level, and retirement plan. This guide may differ between the two, the proper decision, and strategies to ensure that you maximally preserve your savings in 2026.

An Overview of RRSP vs TFSA 2026

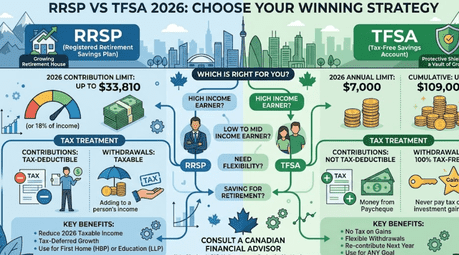

What Is an RRSP?

Registered Retirement Savings Plan (RRSP) is a plan legislated by the government for Canadians that is for retirement savings. Your contributions to RRSPs are tax-deferred in any given year since they decrease your taxable income. In addition, all investments inside the RRSP grow tax-free until withdrawn, usually upon retirement, because at that time your income is most likely lower, alongside the tax rate.

RRSP 2026 Highlights:

- Contribution limit – 18% of the previous year’s income to a maximum of $31,560 for 2026.

- Tax-deferred growth on investments.

Accessibility to utilize programs such as the Home Buyers’ Plan (HBP) and Lifelong Learning Plan (LLP) for selected withdrawals with no tax penalties to be charged immediately.

What is a TFSA?

Tax-Free Savings Account, or TFSA, is another tax-efficient account for Canadians to capitalize on tax-free income. A TFSA account is on the flip side when compared to an RRSP, just in the sense that TFSA contributions are not tax-deductible, but with the promise that all funds from the account are tax-free in the future.

2026 Capped TFSA Attributes:

- Contribution limit: $6,500 annually (2026) for the current year; a cumulative-yearroom allowance is available if you’ve not contributed before.

- The tax-free growth and withdrawals.

- Re-deposit option of funds at will within future years.

RRSP vs TFSA 2026: Key Differences

| Feature | RRSP | TFSA |

|---|---|---|

| Tax Deduction | Contributions reduce taxable income | No tax deduction |

| Tax on Withdrawals | Taxable as income | Tax-free |

| Contribution Limit | 18% of previous year’s income (max $31,560) | Annual limit $6,500 (2026) |

| Best For | High-income earners, retirement savings | All Canadians, flexible savings |

| Government Programs | HBP, LLP | None specific, but very flexible |

Understanding these differences is essential when deciding which account fits your 2026 financial goals.

Why RRSP Will Work for You in 2026

RRSPs are great for Canadians willing to take advantage of their taxable income now while saving for retirement. The following are a few cases where an RRSP is advantageous:

- High-income earners: The higher you earn, the more tax savings you enjoy by contributing to an RRSP.

- Retirement planning: It is the kind of incentive in RRSPs that encourages long-term savings, and the growth deferral on all the tax helps you to build up your old-age nest egg well.

- Home buying or educational purposes: RRSPs enable emergency withdrawals for HBP or LLP and credit the taxes in the future.

RRSP Contribution Strategy for 2026

- By all means, contribute heavily to the RRSP if you can hit a higher income tax rate.

- Donating to the RRSP as soon as the year starts maximizes growth through tax deferral.

- A contribution to the RRSP is meant to reduce the total taxable income at the end of 2026, which might also imply a proper refund on the tax due.

Why TFSA Might Work Better for You:

For its flexibility and tax-free growth, TFSAs are well-liked by Canadians from all walks of life. Benefits include the following:

- For taxpayers earning all kinds of income, as contrasted with the RRSP system, where contributing depends on your income.

- It holds good for either short- or long-term goals like saving for emergencies, holidays, or large item purchases.

- Enjoying the benefits of tax-free withdrawals makes it a smart choice for adding a further top-up to one’s retirement income.

What to Follow in 2026 as Far as Achievement by TFSF?

One must not miss the $6,500 annual limit in their contribution to TFSAs.

One needs to invest in growth-type assets in order to have the benefits of tax-free compounding to the maximum.

Have your earnings on withdrawals reinvested back in following years to further benefit from not losing out on contribution room.

RRSP vs TFSA 2026: Which One Is Best for You?

The decision between RRSPs and TFSAs depends on your income, savings goals, and tax strategy.

- For people with high incomes (in the 40%-plus tax bracket), the RRSP-tax deduction probably outweighs the TFSA’s flexible withdrawal tax-free structure.

- For anyone in a lower to average income bracket or for retirees, who may depend on cracking well before the retirement age, a TFSA might actually benefit.

- Product-specific savings: TFSAs are ideal for short-term ambitions, while RRSP allows long-term investment in the pension.

Ideally, in the case of fiscal year 2026, the most promising maxim is:

Max out your RRSP to save tax effectively if you’re making one hell of an income and if you’re steaming under the collar with worrying about your 2026 tax bills.

Get your TFSA contributions if you want them paid out at any time: for this fund, growth for investments, and for the supplemental retirement.

Make a sound investment: Spread your dollars over an array of ETFs, mutual funds, and high-interest savings accounts available within RRSPs and TFSAs for your growth.

The double-sided approach then achieves the best benefits from tax deferral and tax-free growth.

Tax Implications: RRSP Vs TFSA 2026

So here comes a quick guide to really defining what the taxation in RRSP and TFSA amounts to, to aid you in maximizing your savings levels.

All RRSP withdrawals are subject to income tax. For an illustration, hypothetically take a situation in which you draw out $20000 in retirement, which would then be taxed at approximately 20% to 30%, along with an explicit percentage of the tax taken, of course.

On the other side, TFSA withdrawals are totally tax-free at any growth, whereupon investments can sit.

Planning to apply the potential amendment to the tax bracket and allowance in 2026 would save one a bundle in the name of scores of taxes.

RRSP vs TFSA 2026: Growth Potential

Consider earning a simple 5% for growth after 10 years in the following scenario, as if a $10,000 was invested:

- RRSP: A $10,000 goes for making in a tax-deferred zone up to about $16,300, subject to taxes on withdrawals based on your income.

- TFSA: An amount of $10,000 grows to approximately $16,300 and comes out of the account, thereby tax-free in terms of taxes.

- The main difference comes with the payment of taxes: RRSP postpones the process, TFSAs permanently expunge liabilities.

Tips to Maximize RRSP and TFSA in 2026

Get an early start: The more time you give to contributions equals more interest in your favor due to compound interest.

- Regular contributions: The more frequently scheduled contributions are made, it eliminates lapses in consistency.

- Tax bracket: If you’re in the higher tax bracket, think about maximizing your RRSP contributions.

- Check the TFSA space: It can be uncontaminated by penalties or other things when indexed queries grow faster from going over your account’s limits and generating void transactions.

- Differentiate your investments: For RRSP and TFSA, a strategic blend of equities, bonds, and ETFs can make all the difference.

Common Mistakes Canadians Make

- Overcontributing to a TFSA, inviting penalties.

- Withdrawing prematurely from an RRSP without using HBP or LLP.

- Failure to contribute to the limit.

- Choosing a preferred account in the absence of consideration for the long-term growth and tax strategies.

The avoidance of these pitfalls in 2026 can increase one’s overall financial security significantly.

RRSP versus TFSA 2026: Conclusion

In 2026, Canadians now have more options than ever to save, invest, and grow wealth. While RRSPs can help decrease taxable income and accumulate retirement savings, TFSAs provide flexibility and ensure tax-free growth to accomplish both long- and short-term financial goals.

- The smartest approach often combines the two accounts:

- Utilize RRSPs for tax minimization and retirement savings.

- Use TFSAs for liquidity, emergencies, and tax-free withdrawals.

Come 2026, by understanding the finer points of RRSP versus TFSA, Canadians can really take it upon themselves and make the best-informed decisions to give their investments the best chance to help secure their financial future in this country.